Mobile banking has woven itself into daily life, with millions worldwide tapping their phones to check balances, transfer funds, and pay bills. As this shift deepens, questions around security rise with it. The evolution of digital identity verification is central among the tools banks use to fend off fraud and keep accounts safe.

Watching the Puzzle Pieces Align

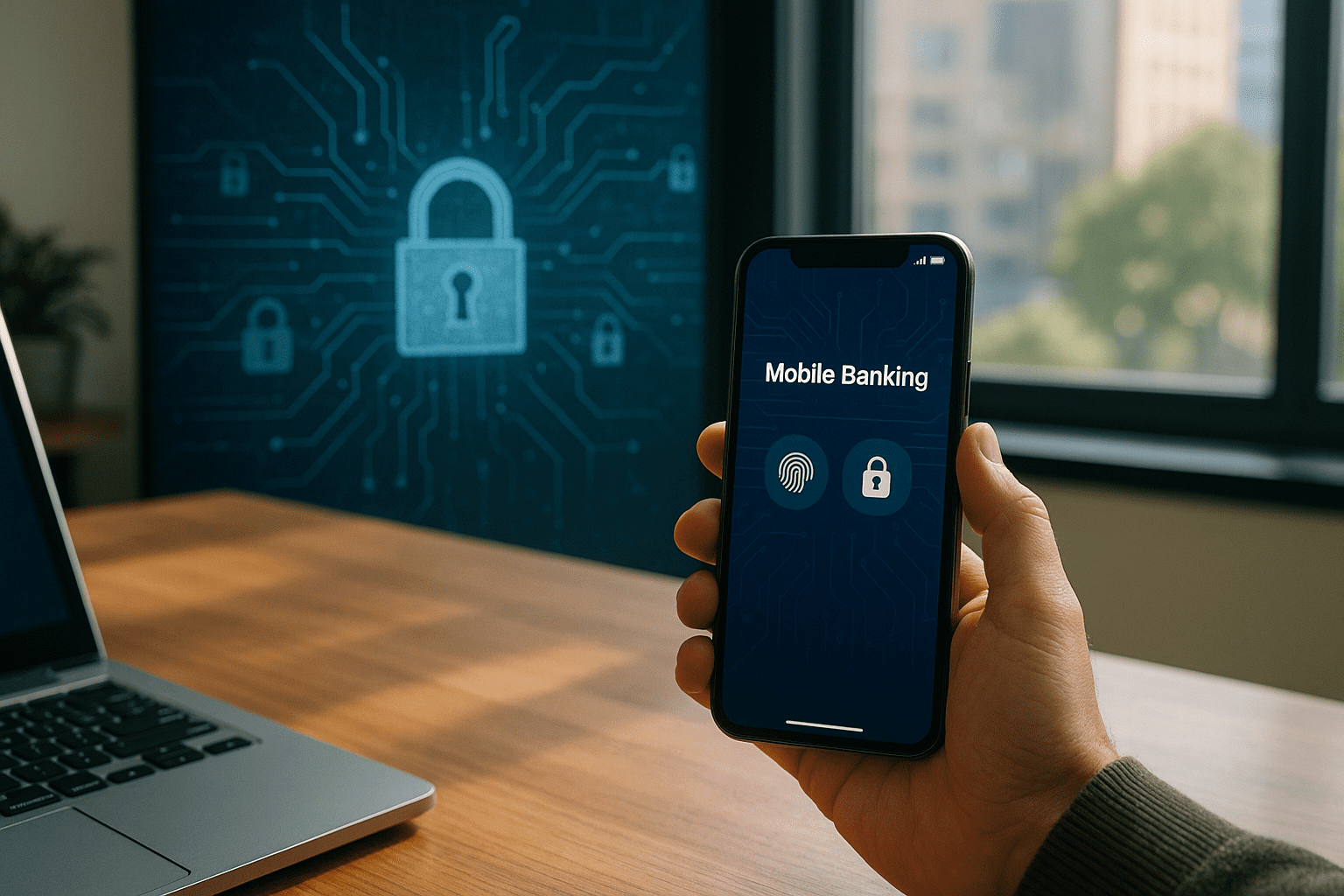

Security in mobile banking feels like a constantly moving target. Fraudsters adapt quickly, chasing new vulnerabilities as technology evolves. In this space, digital identity verification has become a crucial safeguard. It extends beyond traditional passwords or PINs, moving toward something that feels almost personal.

Voice recognition, facial scans, and fingerprint checks increasingly authenticate users. These biometric methods are far from new inventions, yet their integration into mobile banking apps has accelerated. Banks rely on a mix of technologies to verify identity without overly burdening users with complexity. Yet, this doesn’t come without challenges.

Biometric authentication can reduce certain risks, such as stolen passwords or phishing attacks. However, skeptics note concerns about data privacy and the risk of biometric data theft. Unlike a password, you cannot simply change a fingerprint or a face scan.

Still, institutions like the Consumer Financial Protection Bureau highlight these tools as part of a layered defense strategy to improve overall security.

When Convenience Meets Security

Beyond just safety, digital identity verification changes how people experience mobile banking. The balance between convenience and protection is delicate and often influences customer satisfaction.

Many users expect instant access with minimal friction. Methods like biometric logins answer this desire elegantly, replacing cumbersome password inputs with a quick fingerprint touch or glance. This ease can also discourage risky behaviors like password reuse or writing down credentials.

However, not every user has a phone capable of advanced biometrics, or they may hesitate to use them. Banks try to accommodate by mixing options, allowing facial recognition, PINs, or one-time passcodes. A recent survey covered by BankInfoSecurity reveals users appreciate this flexibility, though preferences vary significantly by region and demographic.

Looking Beyond the Screen

Identity verification technology keeps extending past the device into the broader digital ecosystem. Behavioral biometrics, which analyze patterns like typing rhythm, swiping gestures, or device handling nuances, are emerging as less intrusive methods of confirming a user’s identity.

This approach can run passively in the background, spotting suspicious changes that might indicate fraud. For instance, a login attempt that diverges sharply from a user’s usual behavior might trigger additional security steps.

Financial institutions often combine these subtle signals with other data points, including device location and network characteristics. The goal is to catch fraud early while preserving smooth user interactions when all signs point to legitimacy.

Such advancements sometimes rely on artificial intelligence and machine learning. While these tools can detect anomalies in real time, they also require ongoing tuning to avoid false positives that frustrate customers.

The New Frontiers for Regulation and Trust

Regulatory scrutiny keeps pace as banks deploy advanced identity verification tools. For instance, frameworks like the European Union’s Payment Services Directive 2 (PSD2) mandate strong customer authentication to reduce fraud risk.

In the United States, agencies including the Federal Trade Commission and the Office of the Comptroller of the Currency oversee rules impacting digital banking security. Their guidance encourages institutions to adopt a risk-based approach rather than relying solely on prescriptive checklists.

Users remain at the center of trust in these systems. Transparency about how data is collected, stored, and used helps build confidence. The Electronic Frontier Foundation frequently weighs in on privacy concerns, reminding both users and providers to remain vigilant.

This balancing act between innovation, security, and privacy will shape how mobile banking evolves in the years ahead.

Expectations Meet Reality in Everyday Use

People’s experiences of mobile banking security rest on a complex mix of invisible technology and visible trust. When a biometric scan works seamlessly, users may feel reassured. Yet, a single failure to authenticate can lead to confusion or doubts.

Incident response times, customer support quality, and communication about updates or breaches also influence the sense of safety. This human element remains essential as technology advances.

Watching these trends unfold suggests one takeaway: the future of mobile banking security will likely continue weaving technology with thoughtful design and policy frameworks. That combination shapes a landscape where people feel protected without sacrificing ease of access, even as fraudsters find new angles.

In the meantime, individuals can benefit by staying informed about the options their banks offer for identity verification and seeking clarity on how their data is protected. Such awareness complements the efforts banks make behind the scenes.

Mobile banking is a rapid, ever changing realm. Digital identity verification stands as a frontline of defense and a lens through which the evolving relationship between technology, trust, and user experience becomes visible.

For further insights on this, the FDIC’s fraud prevention resources provide clear advice for consumers navigating mobile security.

Meanwhile, ongoing news from industry observers like American Bankers Association shares updates on best practices and regulatory developments shaping this space.

The pace of change may feel dizzying, but the core goal remains constant: helping people manage money confidently and securely wherever they are.

Sources and Helpful Links

- Consumer Financial Protection Bureau, government agency offering guidance on consumer financial security

- FDIC fraud prevention resources, advice on avoiding bank fraud and scams

- American Bankers Association, industry group providing insights on banking trends and security

- BankInfoSecurity, news and analysis focused on banking cybersecurity

- Electronic Frontier Foundation, nonprofit defending digital privacy and security