Financial institutions have long faced cybercriminals relentlessly probing their defenses, but the nature of these threats continues to evolve in complexity and scale. Simple passwords, once a staple of online security, now feel woefully insufficient in a landscape rife with stolen credentials and automated hacking tools. The digital world that banks operate in is not just about technology anymore; it hinges on understanding patterns of human behavior and crafting protections that keep pace with rapidly shifting dangers.

The Shift From Passwords to Continuous Identity Checks

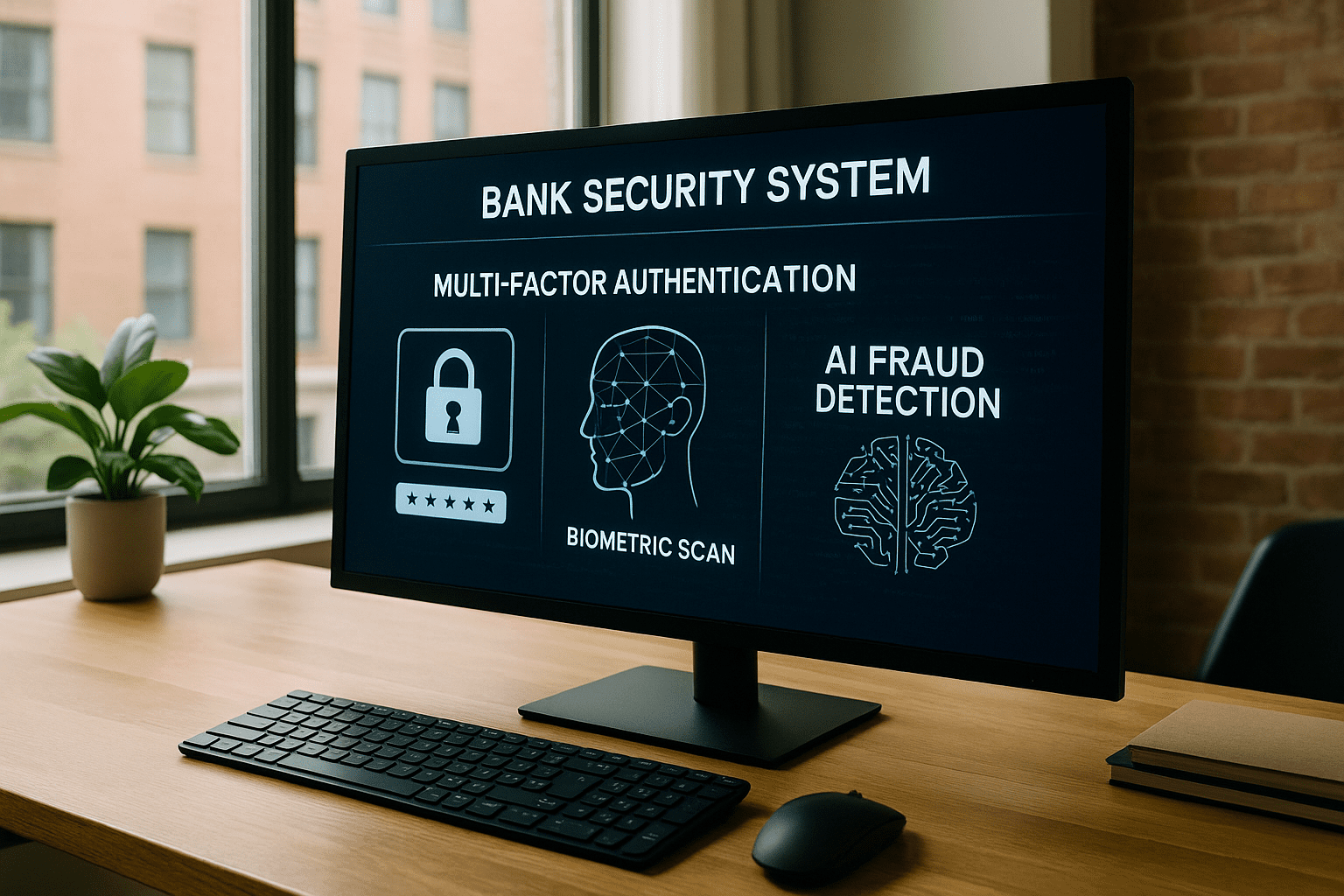

Passwords remain a part of the security picture, but most banks recognize they need more. Multifactor authentication has become standard practice across many institutions. This method asks users to provide two or more pieces of evidence before access is granted, such as a password plus a text message code or a notification from an app. Though some customers might see this as an inconvenience, it makes unauthorized access significantly harder.

Biometrics add another layer to this, leveraging what is inherently unique about a person. Fingerprint sensors on smartphones or facial recognition software are now common tools that banks have integrated, combining user convenience with high security. They reduce the risk connected to stolen passwords while making it smoother for customers to authenticate their identity.

This transition to more dynamic verification reflects a larger trend in cybersecurity that favors continuous assessment rather than a one-time checkpoint. Banks want to be confident not just at login, but throughout the user’s session, monitoring signs of suspicious activity in real time. This approach acknowledges the ways criminals adapt and slip through traditional barriers.

Detecting the Unusual in Everyday Use

Artificial intelligence tools deployed by banks track a wide array of behavioral clues. The system keeps a close eye on where customers usually log in from, which devices they trust, and the ways they typically move money. Any shift from this pattern can trigger alerts for further investigation or additional verification steps before allowing transactions to proceed.

These intelligent systems can spot signals like an unexpected transfer to a new recipient or an unusually large withdrawal. They operate quietly in the background, often catching fraudsters who try to mimic normal customer behavior but fail to match subtle cues. This kind of proactive monitoring is a big leap from simpler rule-based systems of the past and illustrates how banks are harnessing technology to stay a step ahead.

Guidance from the Federal Financial Institutions Examination Council pushes institutions to improve these defenses continually. The council’s frameworks emphasize adaptive risk management and recommend integrating updated threat intelligence into detection systems.

Teaching Customers to Recognize the Threat Landscape

Despite advances in technology, human error remains a significant risk. Fraudsters often start by targeting the end user, sending phishing emails, making fake calls, or setting traps that rely on trust and distraction. Banks have learned they cannot rely solely on technology to keep customers safe; education plays a vital role.

Many banks now offer resources designed to help people spot fraud attempts. From brief warnings during logins to interactive tutorials and simulated phishing tests, these efforts build customer awareness. The idea is to empower users to spot suspicious activity and take protective steps rather than feeling helpless or overwhelmed.

Helping customers become active participants in security strengthens the overall ecosystem. Recognizing the common characteristics of scam messages, such as urgent demands or unusual requests for information, can prevent many attacks from succeeding in the first place.

Security as a Collective Endeavor Across the Industry

No bank is an island when it comes to cybersecurity. Sharing information about new threats and attack methods is crucial in mounting an effective defense. Organizations like the Financial Services Information Sharing and Analysis Center (FS-ISAC) facilitate this by creating a channel for financial institutions, government agencies, and law enforcement to exchange up-to-date intelligence rapidly.

This collective vigilance means that when one bank encounters a new malware strain or phishing campaign, others can be alerted before they face the same risks. Collaboration also extends to best practices for responding to incidents, coordinating law enforcement efforts, and pushing for stronger regulatory standards.

These real-time networks of information reflect the interconnected nature of the financial system. A breach at a single institution can ripple through payment systems, affect other banks’ customers, and undermine trust industry-wide. Shared defense strategies help mitigate these cascading dangers.

The Rising Importance and Cost of Cyber Defenses

Investment in cybersecurity is growing substantially for banks of all sizes. The toolbox now includes more than traditional firewalls or antivirus software. Institutions deploy encryption to keep communications and stored data secure, and use advanced analytics to constantly reevaluate risks associated with user permissions and account access points.

Hiring and retaining cybersecurity talent is also a priority. Skilled professionals with expertise in threat analysis, incident response, and system architecture are essential. Their role goes beyond prevention to include forensic work after breaches, understanding attacker methods, and helping design future defenses. The labor market for these roles is highly competitive, highlighting the strategic value financial institutions place on security staff.

This ongoing commitment to security infrastructure and people reflects the reality that cyber threats represent a persistent and evolving challenge. For customers, this may mean encountering new kinds of authentication steps or security messages. Such inconveniences come from hard-earned lessons about what is necessary to protect sensitive information in an environment where attackers constantly innovate.

Ultimately, banks deploy a layered security model combining technology, people, and partnerships. This approach matches the web of risks stemming from digital banking, emerging technologies, and the human factor. It also recognizes that the financial system’s resilience depends on adapting swiftly to new threats as they arise and maintaining customer trust at its core.

While no security measure can guarantee full protection, the financial industry clearly understands the stakes are higher than ever. The new security protocols reflect a practical, ongoing effort to keep pace with cyber threats, protect assets and identities, and sustain the trust essential for the economy’s smooth operation.

Sources and Helpful Links

- Federal Financial Institutions Examination Council, guidance on bank cybersecurity risk management

- Financial Services Information Sharing and Analysis Center (FS-ISAC), industry collaboration on cyber threats

- American Bankers Association report on cybersecurity, insights and statistics on recent attack trends

- FTC consumer resource on phishing scams, tips on identifying common fraud tactics