Life insurance occupies a unique position within household finances. It represents a long-term promise, a shield for loved ones, but also a contract that can evolve slowly and with little fanfare. Many policyholders rarely encounter the details of changing terms until a new premium statement shows a number that feels unfamiliar or a benefit adjustment is mentioned in passing. These subtle shifts matter even if they do not always command immediate notice.

The quiet weight of small changes

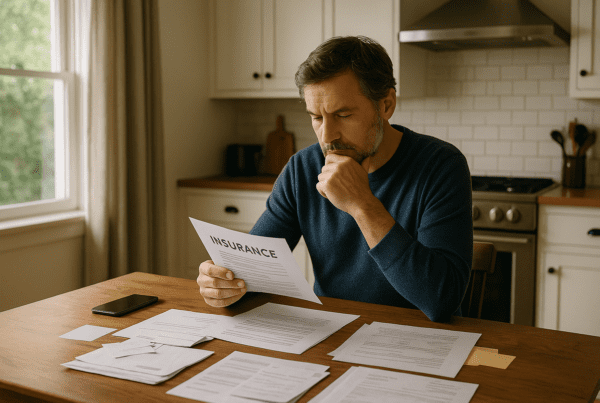

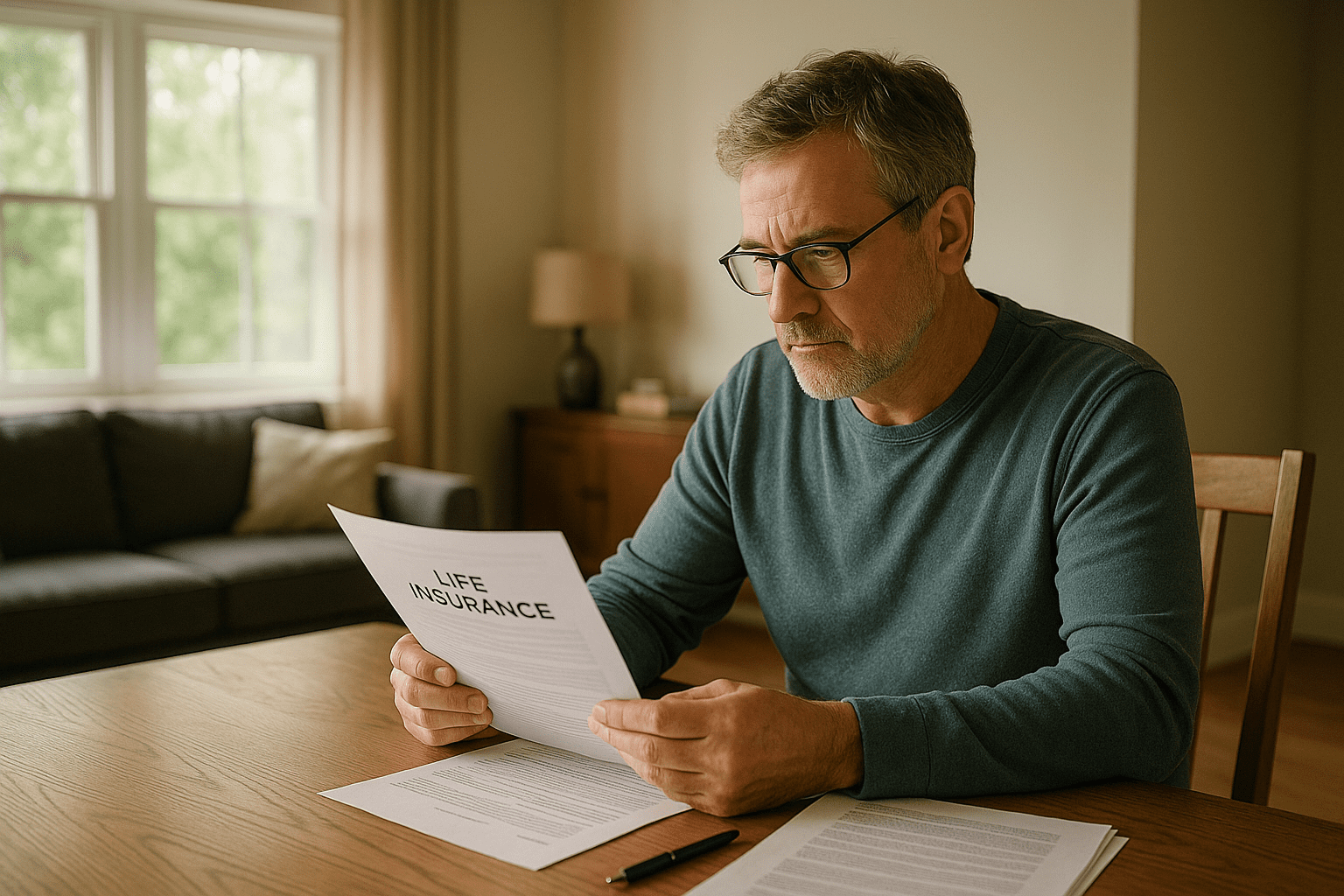

One thing that stands out is how slowly many people actually register term changes in their life insurance. Policy updates travel quietly, often tucked inside annual statements or formal letters. The legal phrasing and fine print tend to discourage a thorough read, leading many to skim or miss the nuances altogether. Those who do spot adjustments might do so only after feeling the pinch of a premium increase or when talking with an agent about their coverage.

This slower realization affects consumer reaction significantly. A surprise premium hike can cause confusion or even distrust, while a mild wording change on coverage might go unnoticed until a claim or life event brings it up. The way insurers communicate these updates plays a crucial role, yet the balance between enough information and overwhelm is a persistent challenge. Efforts to improve transparency have met with mixed results, leaving many consumers uncertain about what exactly has changed.

To add, even well-intentioned communications sometimes land poorly because consumers approach their policies with low expectations of engagement. The perception that life insurance is a distant contract waiting silently backstage until needed means that many are not primed to absorb updates unless something immediately impactful appears.

The fragile trust behind long-term policies

The relationship between an insured person and their life insurance company carries a distinct dynamic. Unlike with other types of financial products such as credit cards or savings accounts, this relationship often stretches over decades and remains largely dormant unless a claim arises or terms alter unexpectedly. The lack of regular interaction can build a fragile sense of trust based mainly on faith in the company’s fairness and stability.

Studies from consumer groups and regulatory bodies, including the National Association of Insurance Commissioners, highlight that unexpected or poorly explained term changes can erode that trust. Feeling blindsided by premium increases or benefit modifications feeds skepticism not only about the insurer but also about financial institutions more broadly. It is a reminder that even small contract evolutions can ripple into larger questions about financial security and reliability.

The challenge extends beyond the contract itself to the overall experience of ownership. When policyholders face unclear messages, a sense of distance can grow. This gulf makes some question their continued loyalty or the true value of a product that changes in ways apparently beyond their control.

How real consumers respond when terms shift

Diving deeper into how consumers react reveals recognizable patterns in their behaviors. Many turn initially to their insurance agents or customer service representatives for answers. When the responses offered are clear and patient, consumers often choose to maintain their coverage despite less favorable terms. That human interaction can serve as a stabilizing factor and build a bridge over the discomfort caused by change.

On the other hand, frustrating or vague explanations tend to prompt shoppers to explore alternatives. Yet the practical realities of life insurance often act as deterrents to switching. Health underwriting complications, new application processes, and potential coverage gaps mean that many people tolerate minor term changes rather than face the uncertainty of replacement. This can be seen as pragmatic inertia where stability matters as much as cost or policy specifics.

Age and policy type influence reactions as well. Younger buyers, especially those with simple term life policies, generally show less patience for obfuscation and are more willing to shop around. Longer-tenured holders of permanent policies demonstrate marked patience, shaped by experience with gradual shifts over years or decades that rarely disrupted their overall coverage plan.

In some cases, life changes such as marriage, home purchase, or parenthood prompt reviews that surface dissatisfaction with evolving terms. These moments provide openings for consumer education and dialogue, though whether they translate into action varies widely.

The uneven rhythm of rules and consumer understanding

The insurance industry operates under a patchwork of state and federal regulations aimed at protecting consumers from unexpected surprises. These rules typically require insurers to notify policyholders about material changes within certain time frames. The intention is to create predictability and fairness, but enforcement and clarity vary widely by jurisdiction.

Organizations like the NAIC provide standardized forms and consumer guides to aid transparency, while many insurers are experimenting with plain language summaries or interactive digital tools to clarify changes. Despite these efforts, a large number of consumers still find it challenging to understand exactly what has shifted in their policies. This ongoing gap suggests that policyholders often piece together information from multiple partial sources rather than receiving a fully clear picture.

The result is an enduring tension between a product designed for long-term assurance and the everyday reality of consumer engagement. Life insurance terms move quietly and incrementally but can provoke significant emotional and practical responses once noticed.

Through regular review, curious inquiry, and trusted advice, consumers may better safeguard their coverage and peace of mind even as contracts evolve in the background. The challenge remains to bridge silence with clarity, so each policyholder can grasp the meaning behind changes and feel confident in their financial protection.

Life insurance itself may shift quietly over time, but the ways people perceive and react to those shifts shape the value it holds in providing financial security over a lifetime.

Sources and Helpful Links