Looking across the landscape of homeowners insurance policies today, it is clear that climate concerns have shifted the playing field in subtle, yet profound ways. What once might have been standard terms and trusted coverage is frequently facing reconsideration as insurers grapple with rising risks related to wildfires, flooding, storms, and related hazards. These changes reveal not only evolving financial calculations but also a growing discomfort with uncertainty in the face of emerging climate realities.

Repricing Risk and Rewriting Coverage

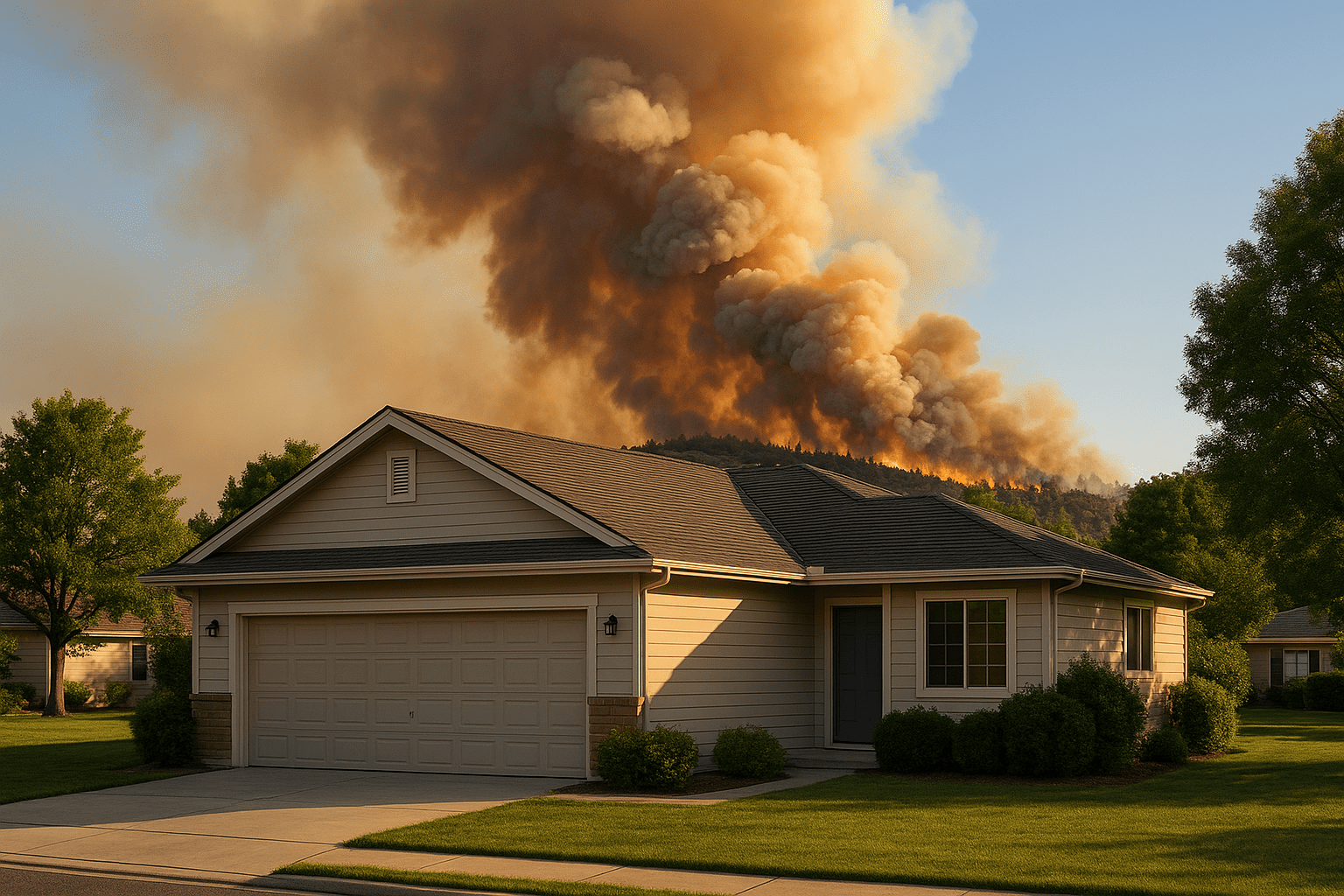

Insurance has always been a business of estimating risk – assigning a price to the chance of loss so that the financial burden, should disaster strike, can be shared. In recent years, the risk profiles for residential properties in many regions have changed markedly due to climate-driven events becoming more severe and frequent. Wildfires in the western United States scorched larger areas than many anticipated, and major flooding events have tested the limits of both natural defenses and insurance frameworks.

As a result, insurers are reassessing what home insurance actually covers and at what cost. Premiums have edged higher in places exposed to recurrent climate threats, reflecting rising claims costs and a reevaluation of risk models. Some insurers have started excluding certain perils altogether or imposing new coverage restrictions, particularly around wildfire damage or flood losses in areas previously considered low risk. This shift has not been uniform across the country, but it spotlights the business adapting to a more volatile environment.

The process is not just about rate hikes. Policyholders may encounter changes to deductibles, where the out-of-pocket expense before coverage kicks in is increased for specific risks. Limited coverage windows or tighter terms for rebuilding or repairs related to climate events are appearing in some contracts. This fracturing of coverage reflects insurers’ attempts to control exposure while maintaining some level of service to customers.

Geographical Pocket Changes and Availability Challenges

It is not just the cost of homeowners insurance that is shifting, but where coverage is offered at all. Insurers limit their footprints based on how climate risk factors affect the likelihood of catastrophic payouts. This phenomenon means homeowners in high-risk areas can find themselves facing limited options or a need to resort to state-backed insurance pools, which often come with their own peculiarities and costs.

Along the coasts and in wildfire-prone zones, we see signs of insurance availability tightening, creating pockets of scarcity. These conditions are particularly stark in California and parts of the Southeast, where homes newly classified as high hazard may face refusals or nonrenewals. State insurance departments, tasked with balancing market stability and consumer protection, are increasingly involved in monitoring these patterns, though solutions continue to be a work in progress.

As these territorial shifts play out, homeowners may have to navigate a complex mix of private insurers, government programs, and sometimes specialized climate risk coverage, each with different rules, costs, and claim processes. This patchwork condition is a far cry from the more straightforward insurance environments many recall a decade ago.

Broader Effects Beyond Pricing and Access

Changes to homeowners insurance policies related to climate risks ripple into broader aspects of homeownership and community planning. Stricter insurance terms can affect mortgage financing, since lenders typically require insurance coverage as a condition of loans. When affordability or availability becomes strained, it may influence housing market dynamics, particularly in climate-exposed regions.

There is also an emerging role for mitigation efforts. Some insurers now offer reduced premiums or improved coverage terms if homeowners undertake certain resilience measures, such as installing fire-resistant materials, improving drainage, or adopting flood-proofing techniques. These incentives reflect a gradual shift from pure risk pricing to encouraging behaviors that stabilize or reduce the chance of loss.

On a larger scale, the evolving picture of homeowners insurance is part of a broader societal reckoning with climate risk. Policymakers, insurers, homeowners, and community planners face the challenge of recalibrating expectations and preparing for a reality where extreme weather is a fundamental ongoing factor, not a rare disruption.

The Data and Models Behind a Changing Landscape

Underneath this observable transformation lies a world of complex data gathering, modeling, and projections. Actuaries and risk analysts are wrestling with uncertainties over how climate change will shape hazard frequency and intensity. This task is complicated by rapidly shifting environmental conditions and the sometimes lagging or incomplete nature of historical data. As highlighted in sources like the National Association of Insurance Commissioners Climate Risk resources, regulatory bodies and insurers are investing more in emerging technologies and collaborations to enhance risk projections.

Such efforts include satellite imagery for wildfire patterns, hydrological modeling for flood risks, and localized climate scenarios to better understand vulnerabilities. Consumers can notice some of this reflected in more frequent policy reviews, requests for additional information on home features, or changes to underwriting guidelines.

The work remains imperfect and shows signs of ongoing adjustment as the new information emerges and climate models evolve. This evolving backdrop echoes a finance sector adapting in real time to one of the most significant environmental challenges of our era.

All told, recent alterations in homeowners insurance illuminate how climate-related risks have moved from peripheral concerns to central forces shaping insurance availability, pricing, and terms. These shifts are ongoing and will likely continue to evolve along with climate patterns, economic conditions, and regulatory responses.

For homeowners, these changes invite close attention, not just to premiums but the fine print of coverage and what protections they can realistically expect. For observers of finance and risk, the shifts offer insight into one corner of how climate transformation translates into tangible effects across everyday financial choices and security.

Understanding these dynamics helps demystify the often complex relationship between climate change and personal finance, revealing a story of adaptation, tension, and cautious recalibration in an uncertain world.

For detailed guidance informed by regulatory insights, the Consumer Financial Protection Bureau insurance section provides clear, consumer-focused information on how insurance works and what to expect when facing coverage changes. Meanwhile, industry analyses such as those from the Insurance Information Institute offer data-driven context on evolving risks and industry responses.

The thread connecting these perspectives is clear: climate risks are no longer background noise but a reshaping force in homeowners insurance, demanding fresh attention to the details and consequences of coverage decisions.

The subtle pressure of change in everyday insurance experience

No one policyholder encounters this shift in isolation. In the lobby of a small-town insurance office or on an online portal reviewing policy options, the cumulative effect of these changes can be unsettling. Rising costs, unexpected exclusions, or the sense that coverage is shrinking quietly push many to reconsider their homeownership risk tolerance or even their plans.

Insurers, for their part, face a balancing act. They must remain financially viable by managing their exposure to catastrophic losses while trying to serve their customer base and comply with regulatory expectations. This tension can result in uneven experiences for homeowners depending on location, home type, and even insurer. Some regions may see stability; others undergo rapid upheaval.

Over time, this unevenness may prompt wider conversations around public policy, infrastructure investment, and community resilience to complement individual insurance solutions. The interaction of private markets, government programs, and consumer behavior will shape how well homeowners can navigate the increasingly complex terrain of climate-related risks.

Ultimately, the journey to adapt homeowners insurance reflects larger societal challenges around living with climate uncertainty, balancing risk and resilience, and finding new pathways forward through changing times.

In this evolving reality, paying attention to shifts in policies beyond the headline premiums becomes a way to understand how climate risk touches down in everyday financial life.

An informed approach means reading past the initial sticker shock to the implications in coverage detail and what that means for protecting a home against a climate-changed future.

As this financial adaptation continues, it shapes not just how people insure but how they live and plan for what lies ahead.

There is no fixed endpoint, only ongoing recalibration as real losses, new data, and changing expectations continue to realign the relationship between climate and insurance.

Sources and Helpful Links

National Association of Insurance Commissioners, climate risk resources

Consumer Financial Protection Bureau, insurance basics and consumer guidance

Insurance Information Institute, climate change and insurance industry insight