The reality of everyday finances has been quietly, then unmistakably, shifting for many households as inflation pressures continue to mount. It is not simply about prices ticking upward. Rather, it is about how those price changes ripple through the choices families make on groceries, utilities, transportation, and even leisure activities. These ripples cause subtle changes that add up to meaningful adjustments in daily life.

The subtle reshuffle of spending priorities

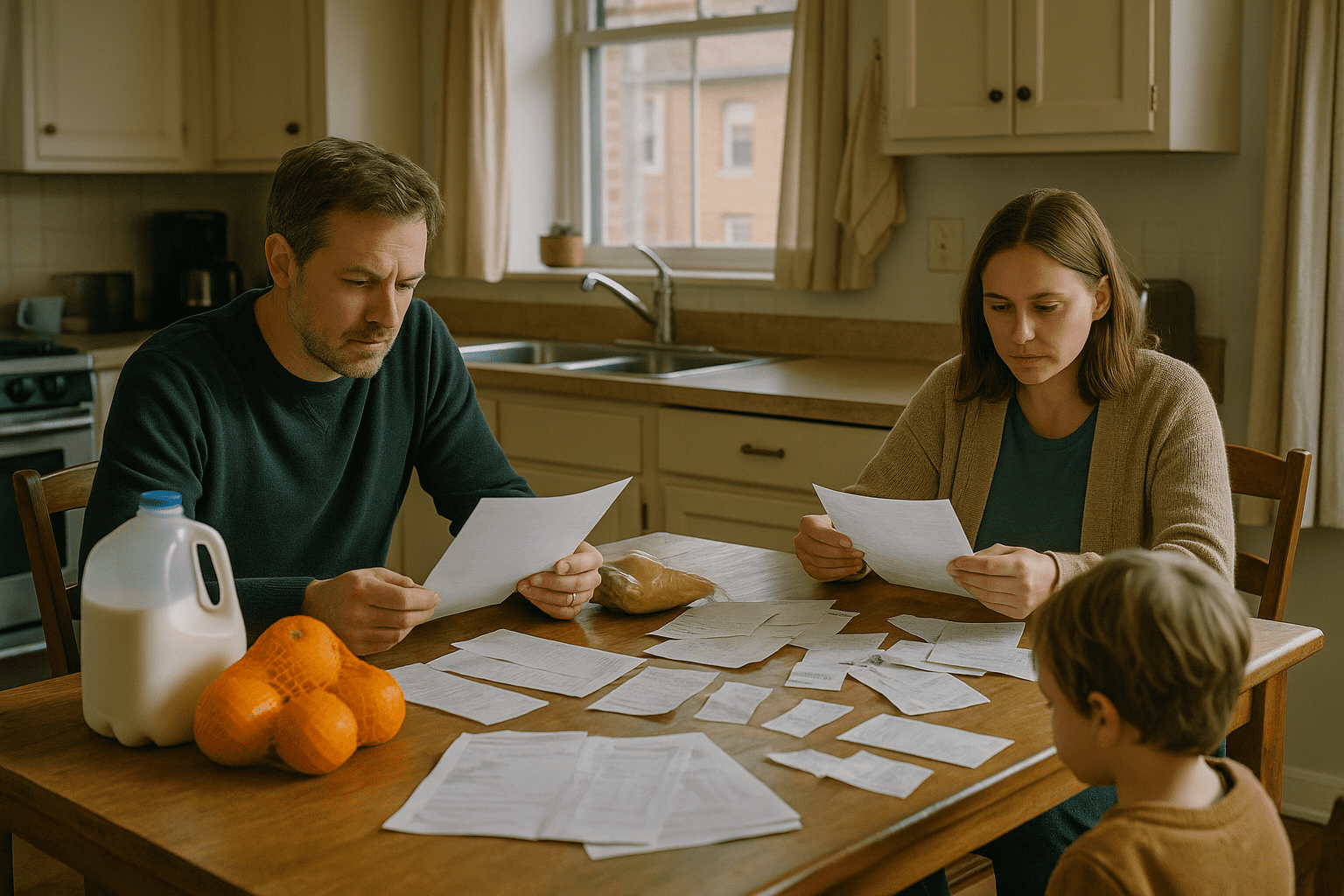

At the heart of the ongoing adjustments is the household budget. For most people, it functions like a living document, constantly nudged and altered to mirror shifting circumstances. Inflation adds a particular strain because it affects categories unevenly. Food prices may climb steadily, while transportation costs spike with fuel prices. Housing-related expenses can take different turns depending on local rents or energy bills. Meanwhile, wages often lag behind these rising costs, squeezing the financial margins.

Groceries, filling stations, and home heating bills represent immediate, pressing parts of the budget. When these costs climb, something has to give. Many households report cutting back on discretionary spending. Restaurant meals come less often. Vacations are postponed or reimagined on tighter budgets. Entertainment expenses are pared down. Smaller scale decisions accumulate, subtly shifting the boundary of what counts as ‘necessary.’

Adjustments ripple beyond immediate expenses to influence how families plan day to day. Bulk shopping gains appeal as a way to lock in lower prices, even if it means upfront cash outlays or more storage space at home. Substituting brands or opting for generic products becomes a common tactic, revealing how price sensitivity grows in everyday routines.

These dynamics play out across income levels but are most acute among middle and lower-income groups. There is less room to absorb extra costs without sacrificing essentials or tapping into savings. Recent figures from the U.S. Bureau of Labor Statistics Consumer Price Index illustrate how inflation impacts categories unevenly, reflecting the lived experience of tightening budgets and rearranged spending choices.

Borrowing, repayment, and the fragile balancing act

Alongside spending adjustments, many households find themselves looking toward credit cards and short-term loans during tight months. But the growing gap between income and expenses makes borrowing more delicate. Interest rates have climbed in recent years as part of economic shifts, and this influences the cost of carrying debt. Paying off bills with credit suddenly comes with extra burdens, prompting a rethink about borrowing habits.

At the same time, moving away from aggressive borrowing does not necessarily translate into quick debt repayment. Instead, some families stretch out payments over longer periods to balance immediate cash flow pressures against longer term financial risk. This creates a layered tension where inflation affects not only what is bought, but also how debt is managed, shaping a complex picture of financial resilience and vulnerability.

Data about household debt service burdens and payment patterns capture this balancing act in motion. According to recent analysis from the Federal Reserve Economic Research, repayment rates tend to slow during persistent inflationary episodes. This trend underscores the challenge households face as they navigate tighter budgets, sometimes at the cost of extending debt repayment timelines or incurring higher interest costs.

Reconsidering savings and emergency cushions

The challenges extend further to savings goals and emergency funds. Inflation eats into the purchasing power of money stashed away, making it harder to preserve wealth through cash savings alone. People respond in different ways. Some try to increase the amount saved to keep up with rising costs. Others, finding immediate expenses overwhelming, struggle to set aside anything at all.

Emergency funds take on greater urgency in periods of economic uncertainty. Job security concerns, unexpected health costs, or sudden home repairs become more worrisome when the buffer provided by savings is shrinking in real value. The idea of having a few months’ worth of expenses readily accessible feels more necessary but also harder to maintain.

Financial advisors often recommend recalibrating savings targets to account for inflation, but this is easier said than done. It involves balancing immediate pressures with future protection, a negotiation many households navigate daily without clear models or guarantees. The Consumer Financial Protection Bureau offers resources for managing such complexity, although the real world often tests even these recommendations.

For some, inflation prompts a shift toward investment vehicles that potentially outpace price increases, but this route carries its own risks and complexities that not all households are equipped to tackle. The tradeoff often boils down to urgency versus security, with savings decisions reflecting a spectrum of comfort with financial uncertainty.

Shifts in well-being and community economies

Over time, the gradual realignment of household budgets reflects deeper changes in overall well-being and economic participation. Reduced discretionary spending can ripple outside the home, affecting local businesses, cultural venues, and service providers reliant on community engagement. Financial stress spills over, influencing health, social connection, and household stability in ways often unseen in aggregate data.

Research from institutions such as the Federal Reserve Economic Research links inflationary pressures to patterns of reduced spending and added financial vulnerability, particularly after sustained periods of price increases. These effects show that budgets are not isolated math exercises but carry implications for social dynamics and economic ecosystems.

Households that manage to adapt well often share common traits: diversified income streams that help spread risk, access to financial products that offer flexibility, and practiced budget management habits that allow for ongoing readjustment. Those lacking these advantages, however, face greater hardship, highlighting the importance of wider systemic supports alongside individual efforts.

The focus on inflation in public discourse tends to center on policy decisions or headline economic indicators. Yet, beneath the surface lies the slower story of daily adjustments at kitchen tables and kitchen counters across the country. These shifts may seem small in isolation but, when added together, signal substantial changes in how money flows through homes, communities, and economies alike.

These patterns offer a reminder that inflation is not simply an abstract economic measure. It translates into countless individual and family negotiations around priorities, risks, and hopes. Understanding how budgets evolve under pressure reveals the true texture of economic life beyond the numbers.

Sources and Helpful Links

- U.S. Bureau of Labor Statistics Consumer Price Index, official inflation data and categories

- Federal Reserve Economic Research, studies on inflation and household behavior

- Consumer Financial Protection Bureau, resources on managing money and credit