The shadow of economic downturns lengthens beyond job losses and reduced consumer spending. One less obvious but significant effect comes through the rise in disability claims. As the economy weakens, more people encounter health or stress-related challenges that complicate their ability to work. This increase carries nuanced financial consequences both for individuals facing heightened pressure and for the disability insurance systems designed to support them.

The subtle ways economic hardship shapes disability claims

Economic slowdowns do more than reduce employment opportunities or shrink paychecks. They create conditions where physical, mental, and emotional strain accumulate. Disability claims often rise in tandem, not simply because of more accidents or illnesses, but due to the greater prevalence of stress, anxiety, and depressive disorders triggered by job instability and financial insecurity.

Studies from credible sources like the Social Security Administration illustrate a clear correlation between unemployment rates and higher applications for disability benefits. This suggests that when workers lose a sense of job security, their health outcomes and decisions about work capacity shift. For some, continued work becomes untenable as stress exacerbates underlying conditions, or mental health issues become overwhelming. One cannot overlook how mental health can sometimes be more debilitating than physical injury, especially when financial worries make rest or recovery elusive.

Access to healthcare also plays a role. During downturns, people may delay or forego treatment due to cost or insurance lapses, leading to worsening conditions that eventually require disability claims. This creates a feedback loop where health problems intensify precisely as financial resources thin. When minor issues snowball into major impairments, claiming disability becomes less about a choice and more a matter of necessity.

Insurance systems under pressure and the impact on premiums

Insurance providers naturally feel the effects of rising claim volumes. Increased payouts push insurers to reassess how they manage risk and price coverage. Group disability plans, often offered through employers, may see premium increases over time. This can lead employers to reconsider plan offerings or adjust employee contributions, complicating access. Employee benefits, which once seemed like a stable safety net, can become more precarious during these times.

On the individual side, planning for such volatility proves more difficult. Private disability insurance policies might carry higher premiums or stricter underwriting during and following economic downturns. Insurers tend to react cautiously to maintain overall fund stability, which might result in fewer options or more exclusions for consumers. People shopping for policies in uncertain economic climates face tougher questions about affordability and coverage adequacy.

The National Association of Insurance Commissioners tracks how insurance regulations and market behaviors evolve alongside these trends. They highlight that while insurers balance sustainability with policyholder protection, navigating these pressures remains a challenge, especially when recessions extend longer than anticipated. Regulatory bodies keep an eye on the delicate balance between keeping claims manageable for insurers and preserving fairness for policyholders.

Balancing individual financial strain with the complexity of claiming benefits

For individuals, the timing of disability challenges during downturns often feels particularly harsh. Lost wages coincide with higher living costs, creating layers of stress. Meanwhile, disability insurance claims usually involve waiting periods before benefits begin. During that time, bills do not pause, and financial pressure mounts. The lag between the onset of disability and receipt of support can be a treacherous stretch.

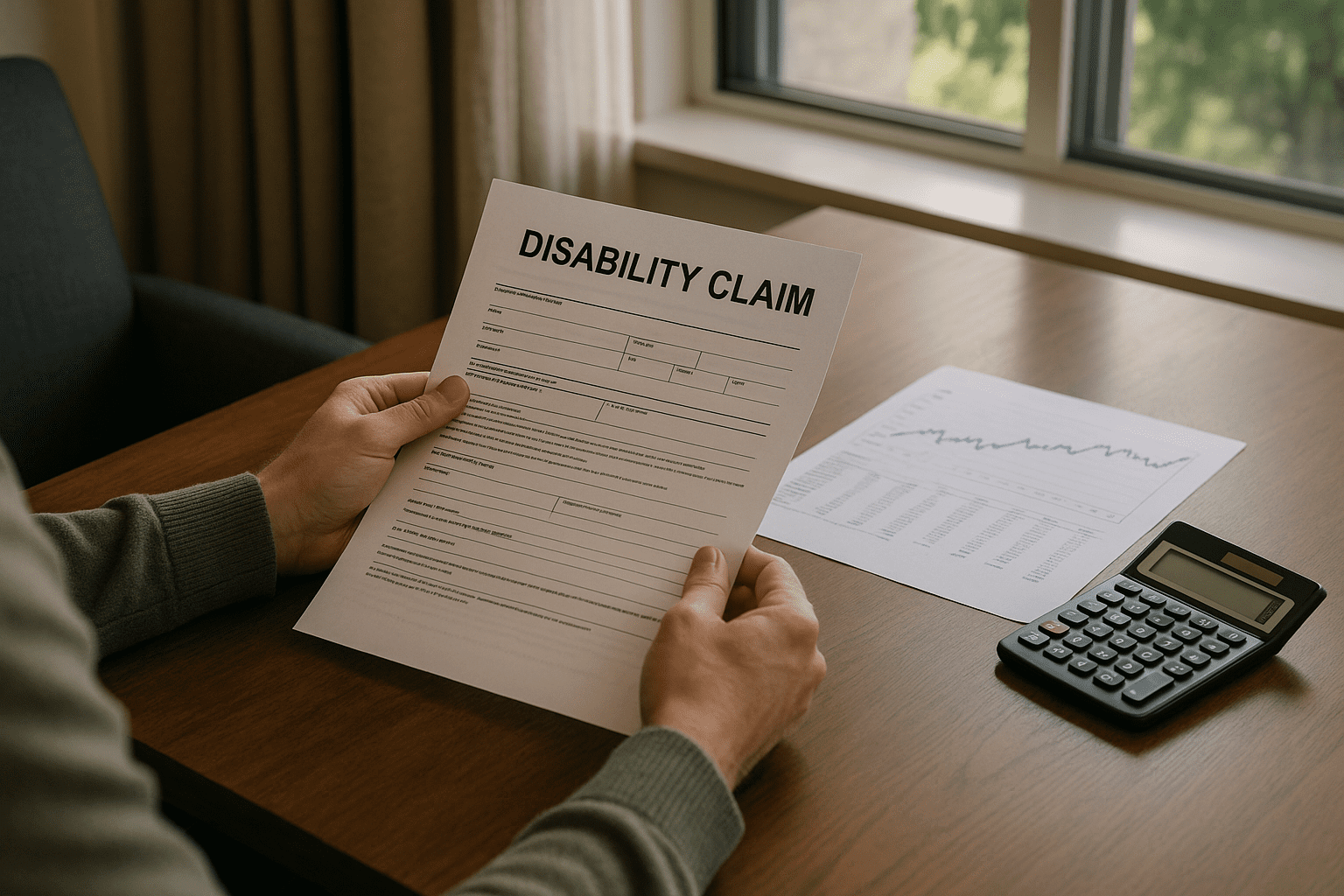

The process of applying for disability benefits is often neither quick nor straightforward. The government’s disability benefits application resource outlines the extensive requirements, which include medical documentation, paperwork, and occasionally appeals. These barriers can disproportionately affect those without savings or support networks, deepening hardship rather than alleviating it. Complex bureaucracies often amplify the vulnerability of those already struggling.

This reality underscores a precarious intersection: people need financial support exactly when accessing it proves most cumbersome. Those without alternate income or emergency funds face compounded risks of falling behind on rent, utilities, or medical expenses, which can influence recovery and long-term outcomes. Such pressures may even push some toward quitting attempts to return to work before they can reasonably manage, risking worsening health or future claims.

Wider systemic cycles and policy challenges

The rise in disability claims resonates beyond individual insurance systems. Public programs like Social Security Disability Insurance (SSDI) may experience additional strain as applications swell during recessions. Already, SSDI contends with funding tightness and lengthy approval timelines. When economic pressures drive more people toward these programs, their capacity to respond efficiently and fairly becomes even more critical. Backlogs and delays frustrate applicants and can erode trust in the system.

At a macro level, higher disability prevalence slows workforce participation, affecting economic recovery dynamics. If a larger share of the population cannot work due to health or stress-related conditions, productivity dips, and the path forward becomes more uneven. This interconnectedness of health and economic cycles shows why public health and economic policy often need to work hand in hand.

This interplay invites more attention to upstream efforts such as workplace accommodations, mental health support, and early intervention strategies. Encouraging employer flexibility or access to treatment can mitigate some claims by addressing issues before they become disabling. While such measures require investment, they can ease downstream financial and social burdens that heavy claims create.

Policymakers face difficult balancing acts. Supporting vulnerable workers without compromising program integrity requires nuanced adjustments in funding, eligibility rules, and benefit design. These conversations become visible especially when economic conditions put pressure on both finances and health across wide populations. Potential reforms often ignite debates about fairness, cost, and long-term sustainability.

Ultimately, the connection between economic downturns and rising disability claims reveals layers of financial risk and resilience. For individuals, it serves as a reminder to consider protections and planning well before crisis hits. For insurance systems and policymakers, it highlights the ongoing need to adapt thoughtfully, seeking to support people without destabilizing the frameworks that serve them. The story is one of balancing immediate needs with long-term health and financial stability in uncertain times.

Many economic recessions are followed by waves of health difficulties complicating recovery beyond pure job statistics. Chronic strain on mental health and untreated physical ailments under economic pressure reveal just how intertwined financial stability and health truly are.

In the evolving landscape of disability insurance, watching these patterns helps explain why claims rise in downturns and why insurance costs and access can feel more volatile than usual. Recognizing these broader connections aids in understanding the daily reality faced by many workers and families in challenging economic periods.

Sources and Helpful Links

- Social Security Administration, research on unemployment and disability claims patterns

- National Association of Insurance Commissioners, overview of disability insurance regulation and consumer info

- Disability.gov, practical guide to applying for disability benefits