Financial planning often gets presented as a tidy process: calculate income, subtract expenses, and set aside savings. Yet when people engage in budgeting day to day, it quickly becomes clear this neat formula usually bends under the weight of real life.

Income level and its stability play outsized roles in shaping how budgets operate. The rhythm of money coming in, the nature of spending demands, and access to financial tools influence not only what budgets look like but also how people rely on them.

Living Close to the Line

For households with limited income, budgeting is less about choosing from options and more about managing scarcity. Paychecks stretch over pressing necessities such as rent, utilities, food, and transportation. Opportunities to absorb financial surprises are rare.

Every spending decision carries a mix of priority and tradeoff. A higher phone bill may lock in essential communication for work, while skipping medical care might seem inevitable yet worrisome. In these cases, budgeting documents do not simply record numbers but trace the fraught navigation through competing needs and occasional compromises.

Income variability deepens these challenges. People paid by the hour or reliant on gig projects often face fluctuating cash flow that makes static monthly plans impractical. Instead, day-to-day adjustments based on actual receipts become a necessary habit. This approach may look erratic from a distance but reflects a careful response to financial uncertainty, balancing known obligations with the unpredictability of what funds arrive.

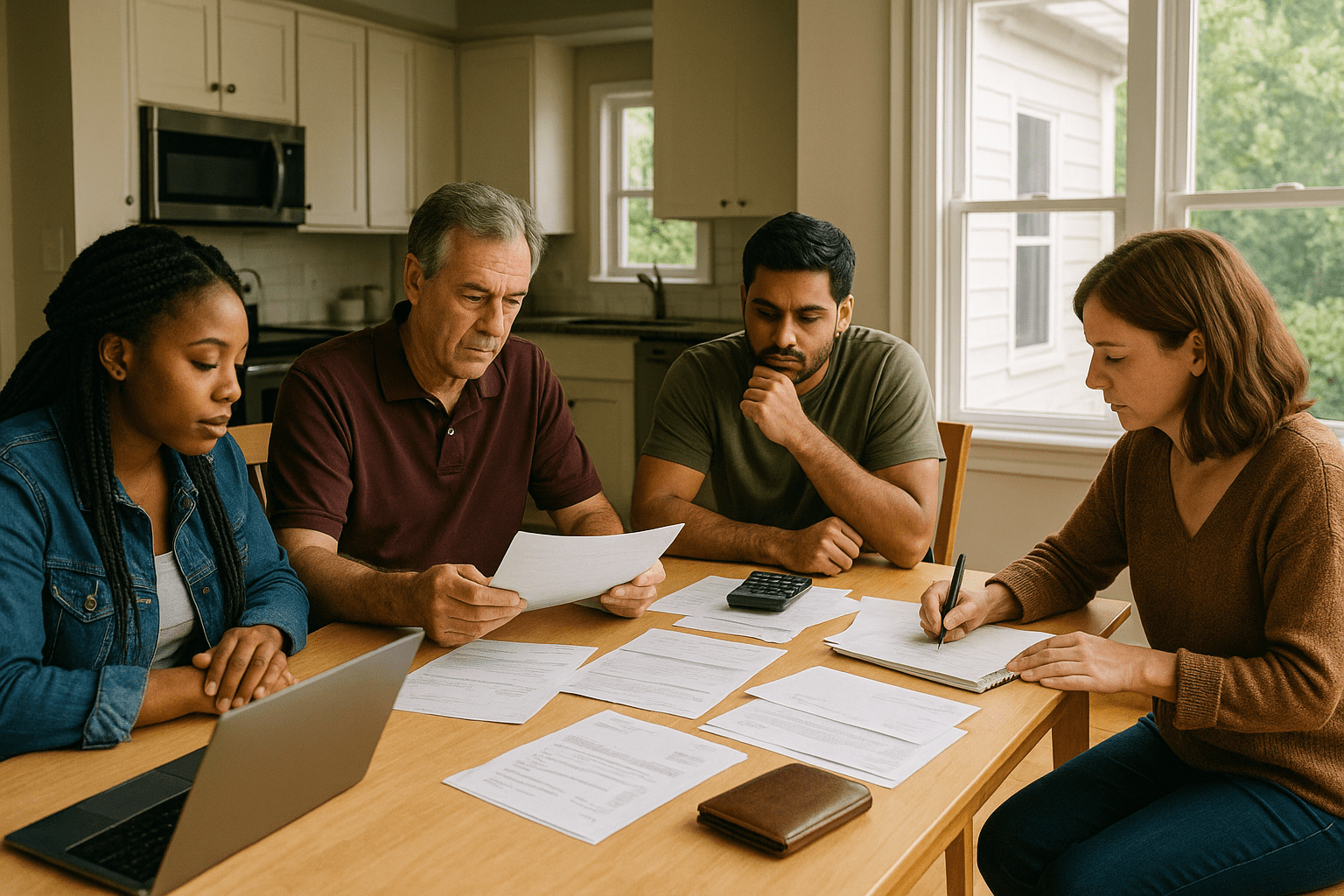

The Middle Income Balancing Act

Households in the middle of the income spectrum often experience a mixture of regularity and disruption. Consistent paychecks provide a foundation for budgeting, allowing monthly breakdowns for fixed expenses such as loan payments or insurance. Yet unexpected costs like car repairs or health bills continue to require flexibility.

These budgets tend to become adaptive frameworks rather than rigid ceilings. Setting firm amounts for essentials blends with ongoing monitoring of more flexible spending categories. This dynamic style acknowledges that while some financial commitments hold steady, discretionary choices and priorities shift with circumstances.

Some mid-income earners adopt a hybrid rhythm: locking in critical budgets but checking in weekly or biweekly to recalibrate spending for dining out, entertainment, or miscellaneous purchases. This reflects the wider experience of managing money with partly stable and partly fluctuating factors.

When Income Enables Strategy and Complexity

At higher income levels, budgeting turns from navigation of constraints to active management of options. Multiple income streams, investments, and financial goals require sophisticated attention. Tax considerations, retirement readiness, and wealth preservation become regular elements of the budget conversation.

Even in this space, discipline remains essential. Budgets address not just current spending but planning for future scenarios, protecting assets, and aligning resources with long term visions. Professional advice and advanced financial tools often enter the picture, enabling more proactive oversight.

While their budgets can be detailed, the underlying principle endures: tailoring management to fit the financial realities faced. Even with more abundant resources, thoughtful decisions on when and how to spend versus save matter greatly.

Financial Access Shapes More Than Income

Income alone does not dictate all budgeting styles. Access to banking services, credit, and financial education also influences how people approach money management. Those with stable banking relationships and financial advice usually find it easier to build budgets that evolve with changing needs.

Conversely, financial instability or the mental burden of juggling unpredictable work and caregiving responsibilities can hinder budget maintenance. In these cases, formal or written budgets may feel less practical, underscoring that effective budgeting often depends on more than just numbers.

Perceiving Budgets as Flexible Tools

Understanding how budgeting practices vary across income lines highlights its role as a living, breathing practice rather than a rigid formula. Successful budgeting often involves negotiation between known commitments, surprises, and shifting priorities.

Advice and financial tools that honor these nuances tend to resonate better with real users. They allow space for imperfection and evolution, meeting people where they are rather than requiring exact adherence to one-size-fits-all templates.

For many, embracing the fluid nature of budgeting means recognizing it as a reflection not just of math but of everyday life realities and choices. That perspective may be key to making financial plans more accessible and sustainable.

Practical insights and tools can be found through sources such as the Consumer Financial Protection Bureau’s budgeting resources. The Federal Reserve’s economic well-being reports shed light on the interplay of income, expenses, and financial stress. Meanwhile, educational content from FINRA helps bridge gaps between financial concepts and everyday practice.

Emerging from the layers of income diversity and situational factors, budgeting appears as a spectrum of approaches suited to varied experiences. Recognizing this helps clear common misunderstandings and fosters more grounded conversations about money.

That realism, in turn, supports people in developing financial habits that better reflect how money really flows and gets used day to day.